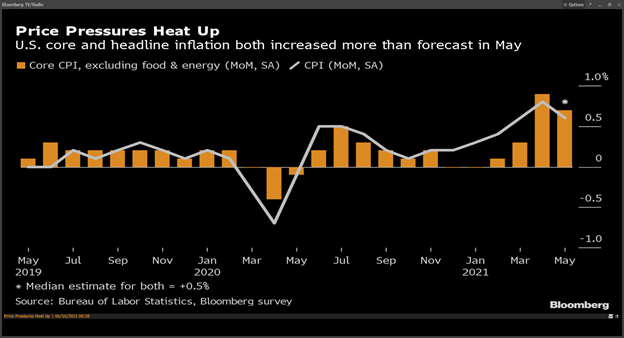

U.S. Consumer Price Index (CPI) inflation increased by 5 percent year-over-year, and 0.6 percent in the month of May - an annual rate of 7.2 percent. The core CPI, which excludes the volatile components of food and energy, rose even faster at 0.7 percent. What popular investment would lose 43 percent if this level of inflation persists?

And can the Federal Reserve and financial markets continue to ignore these inflation readings?

The consensus view is that inflation is transitory, or temporary, and therefore people that are invested in bond and stock markets can safely ignore these elevated readings.

But what if this level of inflation persists?

In that case the markets could be in for a very severe shock if the Fed panics and reverses its interest rate policy of “lower for longer”.

There is a decent argument that this type of inflation is transitory, caused by a shortage of key commodities and goods in an economy that is juiced up by unprecedented amounts of liquidity. In other words, conditions today match the traditional definition of inflation — “too much money chasing too few goods”.

There are some unusual price increases associated with reopening after COVID restrictions:

But the arguments that vehicle rentals and used car prices should not determine the future of inflation may not hold up if the overall trend is persistent and substantial:

This debate matters because the present value of investments is based on the sum of all future cash flows discounted by the cost of money. If the discount rate increases, the present value declines.

Bonds with long maturities are particularly vulnerable. The yield at the long end is only 2.17 percent for a U.S. Treasury note maturing in 2051.

Imagine what investors must believe if they are willing to accept 2.17 percent when inflation is 5 percent!

The long end is distorted by central banks all over the world buying government bonds and keeping interest rates low. Without this steady buying pressure, bond prices would likely fall, and yields would rise. Normally, investors would demand a premium above inflation to lock up their money in a bond that does not mature until 2051.

If the yield on the 2051 maturity bond were to increase to 5 percent the value of that bond would fall by 43 percent.

One of the key elements in the past two decades of inflation has been China’s ability to produce consumer goods at lower and lower prices. This trend may have reversed as the latest report shows a surge in costs, albeit at the factory gate rather than the consumer wallet. The Producer Price Index (PPI) in China surged to 9 percent recently, confirming a trend that started last year:

The Federal Reserve may have the correct view that these pressures are temporary, but evidence is building that inflation is making a comeback.

If the market changes its view, even if the Fed does not, the sell-off in bonds could be violent. And that price correction could hit stock markets and house prices hard.

Hilliard MacBeth

The opinions expressed in this report are the opinions of the author and readers should not assume they reflect the opinions or recommendations of Richardson Wealth or its affiliates. Assumptions, opinions and estimates constitute the author's judgment as of the date of this material and are subject to change without notice. We do not warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Past performance is not indicative of future results. The comments contained herein are general in nature and are not intended to be, nor should be construed to be, legal or tax advice to any particular individual. Accordingly, individuals should consult their own legal or tax advisors for advice with respect to the tax consequences to them, having regard to their own particular circumstances.. Richardson Wealth is a member of Canadian Investor Protection Fund. Richardson Wealth is a trademark by its respective owners used under license by Richardson Wealth.