Canadian banks want the government to take measures to halt the latest surge in home prices.

Several bank CEOs and economists are urging the government of Canada to slow the runaway housing bubble where prices are advancing at a 15 percent annual rate after inflation.

Will the government make bold moves to halt housing mania?

The banks are urging the government to act, but they do not specify exactly what measures they would like to see. The banks are conflicted in several ways.

The housing mortgage business, and related activity, is crucial to the banks’ profits.

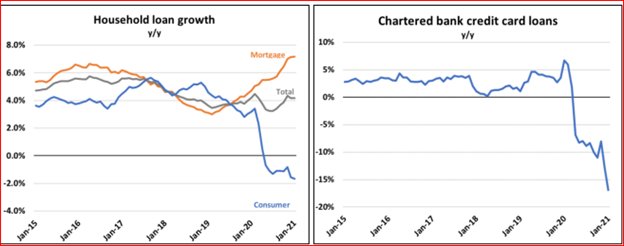

Within the banks, mortgages and HELOCs are the largest share of total loans and management does not want to see a slowing of the growth rate of mortgage loans, especially given the recent slump in credit cards and business loans.

Here is loan growth, courtesy of Ben Rabidoux, North Cove Advisors:

Source: Ben Rabidoux, North Cove Advisors

It is clear that mortgage growth, shown here at close to 8 percent annualized, is key to the banks’ profit growth. Although mortgage interest rates are at record lows, below 2 percent, each bank can make billions of profits in that category, as long as growth keeps up.

Mortgages and HELOCs make up the largest category in Canadian retail lending, by far, accounting for about 60 percent of all assets. For the balance sheet of a bank a mortgage loan is an asset.

So how would the banks like the government to act to slow the rate of increase in house prices, but without hurting their crucial mortgage business?

Robert Kavcic, Senior Economist and Director, BMO wrote a report on March 30, 2021 that contained some suggestions for the government of Canada. “Canadian Housing Fire Needs a Response” is available here.

Some excerpts:

“Policymakers need to act immediately”, “the issue is market psychology”, “break … the belief that prices only rise further”.

Some specific suggestions from the report, ranked by BMO in order of importance:

- The Bank of Canada (BOC) could change interest rate guidance, removing the assurance that rates will stay low for a long time and increase interest rates. BMO sees this as the most important suggestion.

- Change real estate sales process to open bidding.

- Impose speculation tax.

- Increase capital gains tax on real estate.

- Increase supply.

- Impose a non-resident tax.

- Tighten mortgage standards further.

- Limit equity takeout.

- Remove principal residence exemption.

- Help affordability.

To break the current housing market psychology the first suggestion would have a large impact if combined with tighter mortgage standards that reduce demand. But those harsh measures would be highly controversial.

To change the mentality toward housing as an investment there would have to be a significant drop in housing prices (a housing crash), that lasts for five to ten years. This would hurt the economy generally, the mortgage business and bank profits.

No government wants to be responsible for taking the actions that trigger a housing crash.

Watch for tinkering around the edges of the problem, but do not expect bold changes.

Hilliard MacBeth

The opinions expressed in this report are the opinions of the author and readers should not assume they reflect the opinions or recommendations of Richardson Wealth or its affiliates. Assumptions, opinions and estimates constitute the author's judgment as of the date of this material and are subject to change without notice. We do not warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Past performance is not indicative of future results. The comments contained herein are general in nature and are not intended to be, nor should be construed to be, legal or tax advice to any particular individual. Accordingly, individuals should consult their own legal or tax advisors for advice with respect to the tax consequences to them, having regard to their own particular circumstances.. Richardson Wealth is a member of Canadian Investor Protection Fund. Richardson Wealth is a trademark by its respective owners used under license by Richardson Wealth.