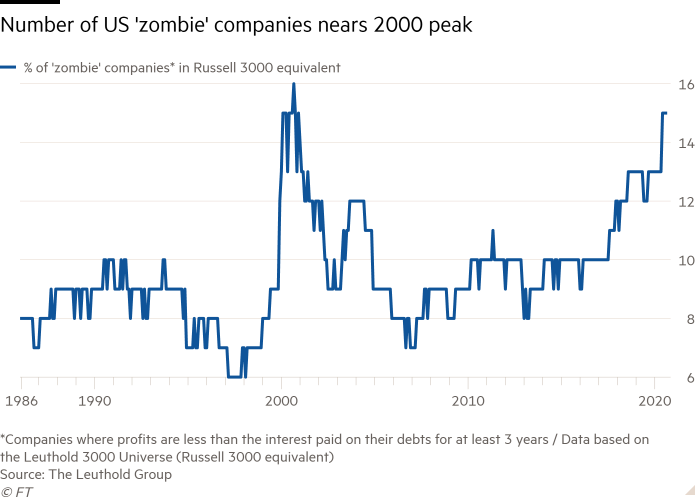

The number of zombie companies is increasing exponentially. As Japan learned in the 1990s, a predominance of companies that cannot pay their debts is bad for the economy.

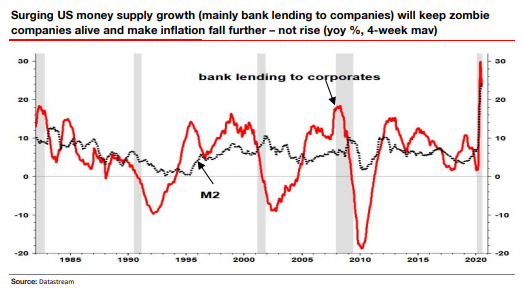

Central bankers kept interest rates unusually low, helping firms stay alive that would have failed even before this recession.

Zombies are a negative force for future growth and innovation.

Source: Adobe Stock

Both the BIS and the OECD have studies showing that zombie companies are a detriment to economic growth, productivity and innovation. Zombie firms are old firms that have persistent problems meeting their interest payments.

“Weak productivity growth is a major problem afflicting our societies. It curbs growth in incomes and endangers the sustainability of our social security systems. An important, but often ignored, source of the productivity slowdown is the increasing prevalence of weakly productive firms and, among them, “zombie firms” – i.e. firms that would typically exit or be forced to restructure in a competitive market” – from the OECD 2017.

The typical zombie firm cannot meet interest payments on its debt, so the bank lender must exercise some form of “forbearance” or the firm will fail. Often firms are “too big to fail” or they are politically connected in such as way that their survival is ensured. In a “free market” firms like these would fail as soon as they were unable to service the interest on their debt.

As many as 16 percent of firms in the broad index, the Russell 3000, are currently unable to meet their debt payments, even with record low interest rates and a junk bond market that is eager to accommodate risky borrowers.

“Ruchir Sharma, chief global strategist at Morgan Stanley Investment Management, estimates that one in six U.S. companies does not earn enough cash flow to cover interest payments on its debt. Such “zombie” borrowers could keep putting off the crunch as long as debt markets kept letting them refinance. But now a reckoning is coming.”

In my book “When the Bubble Bursts: Surviving the Real Estate Crash,” Second Edition 2018, I discuss the theories of Hyman Minsky, an obscure US economist that spent much time thinking about the debt cycles and speculative finance. Minsky says that there are three stages of corporate lending:

First, the “hedge finance” stage means that firms can finance their debt out of income. With profits they can invest in new capital and innovation.

Second, “speculative finance” arrives when income is not sufficient to completely cover interest and amortization of debt payments, but the rollover of existing loans into new loans and rising asset prices keeps the borrower afloat. Banks relax their underwriting standards to allow more innovative methods of finance in order to keep the party going. This stage can last for decades and describes the last twenty years.

And finally, we have “Ponzi finance,” where income is insufficient to cover even the interest payments. This final stage leads to a “Minsky Moment,” where widespread bankruptcies occur, asset prices plummet and a new cycle begins with firms under new management.

Many of the mature firms in developed countries are at the Ponzi phase and have been for some time. The COVID-19 recession means that the crisis that comes with the end of Ponzi finance is here.

During this crisis, many firms will fail. Banks will take huge losses when they admit that some borrowers are insolvent. Thousands of people become unemployed. Governments get voted out because someone must take the blame.

But the only alternative, an endless postponement of the day of reckoning, is worse.

It is crucial for future growth and innovation to let the zombies fail.

Hilliard MacBeth

The opinions expressed in this report are the opinions of the author and readers should not assume they reflect the opinions or recommendations of Richardson GMP Limited or its affiliates. Assumptions, opinions and estimates constitute the author's judgment as of the date of this material and are subject to change without notice. We do not warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Past performance is not indicative of future results. The comments contained herein are general in nature and are not intended to be, nor should be construed to be, legal or tax advice to any particular individual. Accordingly, individuals should consult their own legal or tax advisors for advice with respect to the tax consequences to them, having regard to their own particular circumstances.. Richardson GMP Limited is a member of Canadian Investor Protection Fund. Richardson and GMP are registered trademarks of their respective owners used under license by Richardson GMP Limited.