A full-blown global recession is inevitable at this point, due to government efforts to contain the spread of COVID-19.

The world’s economy was slowing before the pandemic hit. A growth slowdown has now become a widespread economic contraction.

Stock markets reacted sharply with most stocks down at least 30 percent, and some large firms in the energy sector down more than 70 percent. A few investors are already asking if it’s time to invest.

When can we buy stocks again?

One of the best things about the stock market as an investment tool is the rapidity of change. Since the peak in the markets, measured by the U.S. S&P 500 index on February 20, 2020 at 3,380 there has been a 1,000-point drop. This one-third correction happened in the shortest time on record going back to 1926 when the index was first calculated.

On Monday of this week, the index fell by 12 percent, a drop that was second only to the famous crash of October 19,1987. The market recovered by the end of 1987 since that crash wasn’t accompanied by a severe recession. A V-shaped recovery this time is unlikely since most of the world’s economies are in recession along with a bear market in stocks.

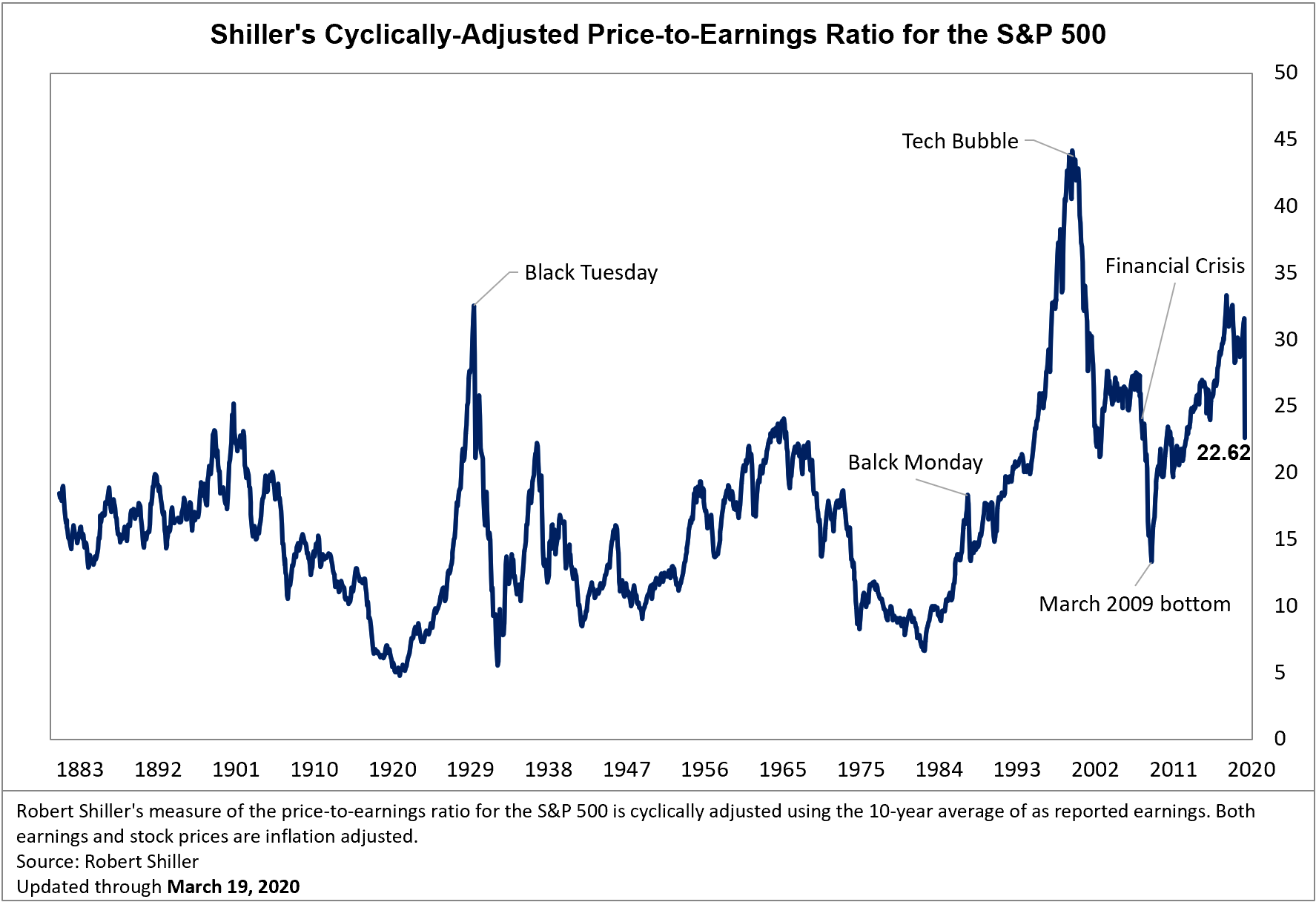

The correction was long overdue. Prior to the recent peak, valuation measures showed that US stocks were as expensive as 1929 and almost as expensive as the dot-com bubble in 2000. Day-trading stocks was an exciting and entertaining pastime in the last few years, but it was dangerous because of expensive prices for almost all stocks.

Paying too much for a stock is a mistake although there is a school of the stock market, called momentum investing, that focuses on trends and not valuation. Another term for that strategy is the “greater fool” theory where a trader knows that it’s foolish to buy a stock at such expensive valuations but there is a “greater fool” coming along behind that will pay an even higher price. Now these “greater fools” have disappeared.

Current valuations are getting closer to reasonable levels, if not yet cheap. Value investing will make a comeback that is long-overdue. Valuation should be the most important consideration for long-term investors.

As of Thursday morning, the US S&P 500 index was back to November 2016 levels when President Trump was elected. All the gains since then have been wiped out by this correction.

Outstanding bargains that often prevail after a market crash haven’t appeared yet for the market indices.

Our favorite valuation tool, the Shiller CAPE, shows the S&P 500 index (and its predecessor) is still expensive, and the bear market isn’t done yet, although valuations are improving.

The median level is 15.77. The chart shows market bottoms in 1982, 1932 and 1920 when the index was below 10. The 2009 bottom didn’t go substantially below the median value.

Traders also watch for signs of capitulation, when nervous investors dump stocks out of fear. This stage is usually accompanied by bad news.

Headlines will be negative over the spring and summer as COVID-19 hits North America harder. The recession that started in Canada in late 2019 will become more severe due to record low oil prices and business closures in manufacturing and services.

Events that accompany market bottoms include bankruptcies in several large corporations, signs of financial stress when highly indebted households start to lose their homes and government bailouts for the financial sector. When announcements like this prevail, the bottom could be near. But always check valuation first.

And remember, it’s impossible to time the market bottom precisely.

Hilliard MacBeth

The opinions expressed in this report are the opinions of the author and readers should not assume they reflect the opinions or recommendations of Richardson GMP Limited or its affiliates. Assumptions, opinions and estimates constitute the author's judgment as of the date of this material and are subject to change without notice. We do not warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Past performance is not indicative of future results. The comments contained herein are general in nature and are not intended to be, nor should be construed to be, legal or tax advice to any particular individual. Accordingly, individuals should consult their own legal or tax advisors for advice with respect to the tax consequences to them, having regard to their own particular circumstances.. Richardson GMP Limited is a member of Canadian Investor Protection Fund. Richardson and GMP are registered trademarks of their respective owners used under license by Richardson GMP Limited.