The era of a comfortable retirement funded by defined benefit pension plans is fading rapidly from the scene in North America. Companies and governments offering defined benefit plans are struggling to fund their obligations. Some have even reduced payments arbitrarily for pensioners and most no longer offer a pension to new employees.

Was the guarantee of a comfortable retirement income too good to be true?

Recently General Electric modified the terms of their defined benefit pension plan, a plan that guarantees a level of income to the retiree. The GE plan is underfunded by 25 percent or about $20 billion. Besides freezing benefits for 20,000 current employees, the company offered a lump-sum payment to about 100,000 former employees. GE also contributed $5 billion to the plan, bringing the pension deficit down to “only” 16 percent of pension liabilities.

In 2014 Jim Leech, retiring CEO of Ontario Teachers’ Pension Plan wrote a report highlighting pension funding issues. Teachers were living about 31 years in retirement to age 90, much longer than the 20 years of pension income received by those retiring in 1970. Teacher contributions made up only 15 percent of assets, with government providing 15 percent and investment returns generating 70 percent. The fund had averaged 13 percent return in 2012, but still had a $5.1 billion deficit.

Days of earning 13 percent returns are over with interest rates at 1 to 2 percent. Either benefits will have to be adjusted lower, or contributions will have to rise. Most pension plans have increased their higher-risk investments, like stocks and real estate, to search for better returns.

For companies with defined benefit plans, underfunding is an even bigger challenge as their cash flow may not allow them to increase their contributions. If they fully fund their pension plan liabilities, they might have to cut dividends. So, most of them just leave a deficit in their funding requirements, until they are forced to contribute more by the regulators. Most companies are trying to get out of offering a defined benefit pension as fast as they can.

The Canada Pension Plan now requires that all Canadian workers contribute a larger portion of their income, up to 5.95%. And employers must match that, making the contributions nearly 12% of income after the changes are fully implemented by 2025. But even with those massive contributions the retirement income from the CPP still might not be enough to live on at age 65.

In 2020, for the first time, Canada Pension Plan payments to retirees will be greater than receipts from contributions. With assets of $392 billion the CPP is not going to be insolvent any time soon. But the fund needs good returns from investments to meet its obligations. With 10% of the fund in real estate, 23% in private equities and 33% in publicly traded equities the pension plan is much more exposed to market risk than a decade ago.

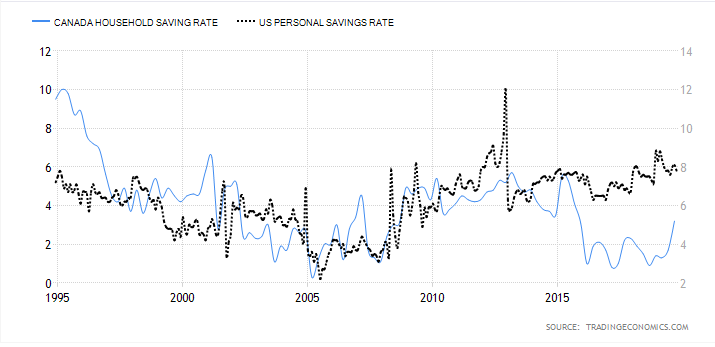

The solution to underfunding is simple. Individual Canadians need to save more outside of government or employer-sponsored plans. But Canadians were saving at the lowest rate in the developed world recently. While Canada’s saving rate averaged about 7.5% from 1961 to 2019, in recent years Canadians have saved much less, preferring to invest in other things, like real estate.

Canada household and U.S. personal savings rates

Source: Tradingeconomics.com

This unusually low savings rate suggests a rebound to higher levels of savings for Canadians is coming. Maybe the surge in late 2019 is the start of a trend.

Higher levels of savings will require sacrifice, in the form of reduced consumption. There is no longer any guarantee of a comfortable retirement.

Hilliard MacBeth

The opinions expressed in this report are the opinions of the author and readers should not assume they reflect the opinions or recommendations of Richardson GMP Limited or its affiliates. Assumptions, opinions and estimates constitute the author's judgment as of the date of this material and are subject to change without notice. We do not warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Past performance is not indicative of future results. The comments contained herein are general in nature and are not intended to be, nor should be construed to be, legal or tax advice to any particular individual. Accordingly, individuals should consult their own legal or tax advisors for advice with respect to the tax consequences to them, having regard to their own particular circumstances.. Richardson GMP Limited is a member of Canadian Investor Protection Fund. Richardson and GMP are registered trademarks of their respective owners used under license by Richardson GMP Limited.