Investment strategies get divided into two camps, growth and value.

Most successful investors like Warren Buffet believe that value investing is better than growth investing.

However, in the last decade, value investing has performed abysmally compared to growth.

Is value investing dead?

A Globe and Mail article in August 2019 is titled, “Five reasons why value investing may never regain its appeal.”

Headlines like this appear near the end of a long trend that is about to reverse. Obviously given the years of poor performance for value investors, many are questioning this approach.

What is the track record for “value investing” versus “growth investing”? Studies by Eugene Fama and Kenneth French show that, from 1926 to 2019, in the US stock market, the category of “equal-weighted small value” had the best performance, at 18.34% annualized. Growth investing, in the category of ‘equal-weighted large growth” earned a much smaller return of 9.56% annualized. The gap in investment gains over the 93 years is enormous. See here.

Over long periods we conclude that value investing is superior in returns, although Fama and French found that those returns came with higher volatility.

Closer examination, according to a study by BCA Research, shows that almost all that excess return from value came in the first 80 years of the 93-year period.

The last 13 years have been terrible for value investing, which is not what was expected after a global financial crisis like the one that occurred in 2008-09.

There are some theories that attempt to explain the recent underperformance in value. The author of the Globe and Mail article suggests that new technology might be the culprit. Almost all stocks in the technology sector are considered “growth”. And technology names, like Amazon, Alphabet, Facebook and Netflix have performed very well.

On the other hand, “value investing” in 1999 saved those of us who avoided the dot-com bubble. In my 1999 book, “Investment Traps and How to Avoid Them”, I suggested that the 1996-2000 dot-com bubble was a “buy-high” trap. It was a painful couple of years for those who avoided that trap but by 2002 they were well-rewarded.

The sentiment today feels like the “irrational exuberance” of the late 1990s as today every investor in an ETF that concentrates on US large-cap growth stocks has returns that are great, while value investors are quietly licking their wounds. One difference in 2019 versus 1999 is that this recent period has lasted much longer.

Most segments of the US market are expensive and there is very little “value” to be found. Berkshire Hathaway, Warren Buffet’s investment vehicle, has a record amount of cash on hand, almost $122 billion. Buffet, the world’s most famous value investor, claims to be looking for an elephant-sized acquisition, but it’s a safe bet that he is horrified by equity market valuations. That pile of cash represents 60% of the total value of his investment portfolio, which is unusual for one who speaks positively of investing in the stock market and denigrates market timing.

In his latest annual letter Buffet says, “Prices are sky-high for businesses possessing decent long-term prospects.”

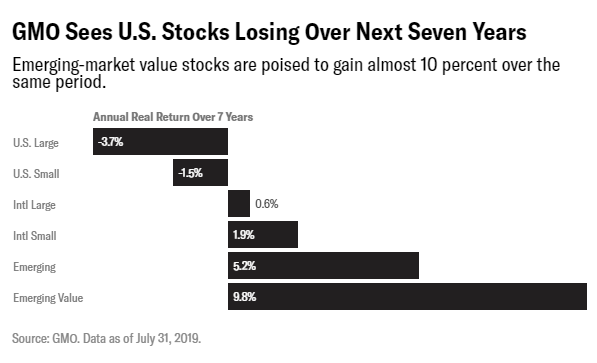

Some attractive value investments can be found outside of the U.S. In the Euro area and emerging markets there are many companies that meet the criteria of a value style of investing. But the investment crowd is hesitant to venture into those “higher-risk” areas.

Sources: GMO and Institutional Investor

Value investing is not dead, but it is testing the patience of investors who are trying to follow that approach. It’s very likely that someday, “value” will make a comeback when people least expect it.

Hilliard MacBeth

The opinions expressed in this report are the opinions of the author and readers should not assume they reflect the opinions or recommendations of Richardson GMP Limited or its affiliates. Assumptions, opinions and estimates constitute the author's judgment as of the date of this material and are subject to change without notice. We do not warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Past performance is not indicative of future results. The comments contained herein are general in nature and are not intended to be, nor should be construed to be, legal or tax advice to any particular individual. Accordingly, individuals should consult their own legal or tax advisors for advice with respect to the tax consequences to them, having regard to their own particular circumstances.. Richardson GMP Limited is a member of Canadian Investor Protection Fund. Richardson is a trade-mark of James Richardson & Sons, Limited. GMP is a registered trade-mark of GMP Securities L.P. Both used under license by Richardson GMP Limited.