Modern Monetary Theory, or MMT, is the hot topic today. MMT has pushed its way to the front of the discussion on the economy and likely will be debated during the Presidential election next year.

At least one well-known money professional, Ray Dalio of Bridgewater Associates, founder of the largest hedge fund in the world, claims that MMT is “inevitable”.

What is MMT? Could MMT be adopted in the U.S.?

According to some, MMT is a “hot mess” of fringe ideas that almost nobody in the world understands. Recently the full theory was laid out in a textbook, Macroeconomics, written by Bill Mitchell, Randall Wray and Martin Watts.

MMT is not easy reading, even for someone who has spent years studying macroeconomics going back to the 1960s. So, it is inevitable that a shortcut version, perhaps incorrect, will be widely circulated and criticized.

Bloomberg published a guide to MMT on March 21, 2019.

According to the authors of the article, MMT says that:

“A country with its own currency, such as the U.S., doesn’t have to worry about accumulating too much debt because it can always print more money to pay interest.”

According to MMT, the only constraint on government spending is the chance that inflation will break out as the government prints and spends more money than there are resources available. MMTers point out that the government can easily fix that problem by increasing taxes to reduce excess demand.

Could there be some validity in MMT?

A leading heterodox economist, Steve Keen, has said many nice things about it. One of the best things about MMT is that it treats banking in a more accurate and realistic way. Traditional theory treats banks as intermediaries between savers and borrowers, a view that has been proven wrong, while MMT correctly describes how banks create deposits and new money when they make a loan.

Here’s Professor Keen presenting to the first international conference on Modern Monetary Theory, held in February 2019.

Ray Dalio recently posted an article on LinkedIn that supports MMT. He says, “the most important engineering puzzle … is how to get the economic machine to produce economic well-being for most people when monetary policy does not work.”

People have noticed that the current system is not working. What central bankers have done for decades is to use monetary policy as the only policy tool, encouraging the private sector to go deeper and deeper into debt to keep the economy growing. But those policies have led to asset bubbles which lead, inexorably, to crashes. And the economy has grown slowly, with gains unequally distributed between rich and the poor.

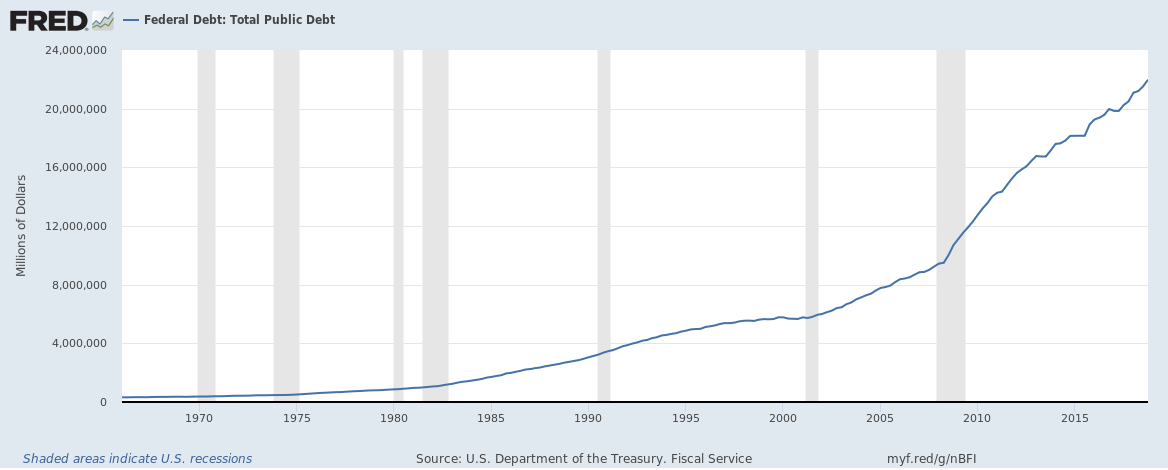

People are looking for alternatives, given this patchy track record. And, in support of MMT, there’s evidence that people are too worried about government deficits. For example, the U.S. government’s debt has grown steadily since 1970.

Source: St. Louis Fed - FRED

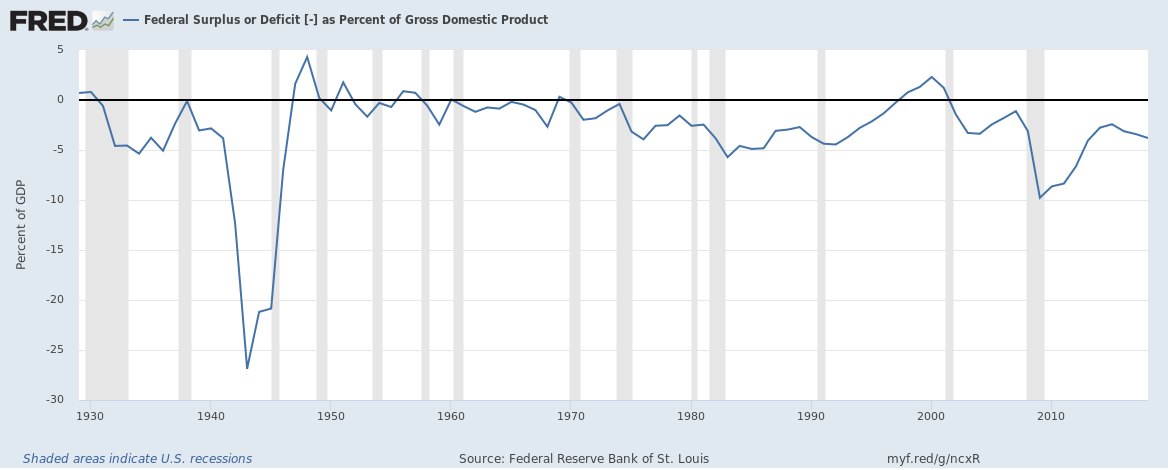

The U.S. government spends more than it receives in taxes, most of the time. So, MMT proponents are right saying that governments can go deeper into debt without worrying about a collapse, at least until now. Here we see that wars have coincided with the biggest deficit in the past hundred years.

The shortcut version: “deficits don’t matter”.

Source: St. Louis Fed - FRED

MMT advocates are focused on the government sector but there’s more to the economy than government spending and debt, which is only about 30% of total spending. The more dangerous types of debt, like corporate loans, mortgages and credit cards given to the private sector, are much more likely to be in default, as we’ve seen countless times in the last century.

The next financial crisis will arrive like the last one, whether MMT is adopted or not, unless we find a way to prevent lenders from providing excessive credit to the private sector during the boom times.

Hilliard MacBeth

The opinions expressed in this report are the opinions of the author and readers should not assume they reflect the opinions or recommendations of Richardson GMP Limited or its affiliates. Assumptions, opinions and estimates constitute the author's judgment as of the date of this material and are subject to change without notice. We do not warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Past performance is not indicative of future results. The comments contained herein are general in nature and are not intended to be, nor should be construed to be, legal or tax advice to any particular individual. Accordingly, individuals should consult their own legal or tax advisors for advice with respect to the tax consequences to them, having regard to their own particular circumstances.. Richardson GMP Limited is a member of Canadian Investor Protection Fund. Richardson is a trade-mark of James Richardson & Sons, Limited. GMP is a registered trade-mark of GMP Securities L.P. Both used under license by Richardson GMP Limited.