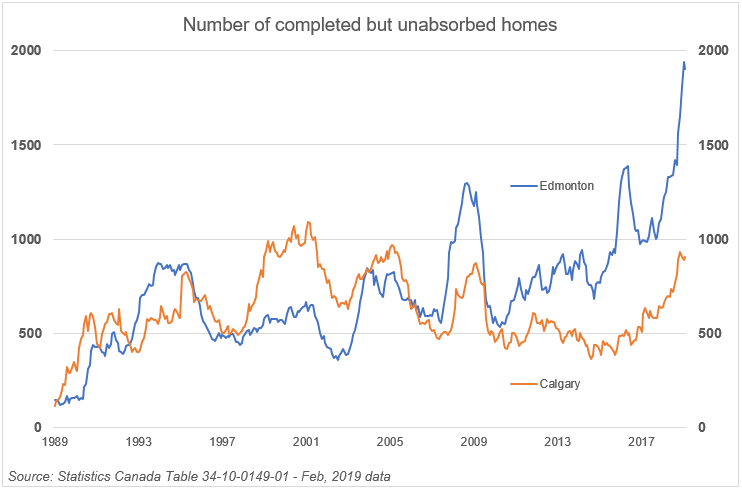

The great Canadian housing correction is well underway. Reports of declines of greater than 20 percent in single family home prices in Toronto and Vancouver are widespread, especially in the more expensive segment of the market. Large supplies of new homes in Calgary and Edmonton are sitting unsold due to a lack of buyers.

My 2018 book, “When the Bubble Bursts: Surviving the Canadian Real Estate Crash”, a completely revised second edition, gives people valuable information about how to survive the bursting of the bubble.

Are Canadians ready for a real estate crash? What can people do to be prepared?

In late 2014 and early 2015, I did my first interviews about the real estate bubble. Most of the questions then were about the bubble: Is it really a bubble? Why does it have to burst? What will be the catalyst causing it to burst?

Now that we are well into the correction, which probably will become a “crash”, people have different questions: Will it be a soft landing? How long will I have to wait for my house value to recover? Is it time to buy, now that prices are lower?

In Part V of the book I give some ideas for people wishing to protect themselves from the fallout of a real estate crash.

Here are a few suggestions:

Don’t be a landlord. Condominiums especially are a terrible investment. The value in real estate is in the land, not the building structure. In high-rise condos most of the purchase price goes to items like the cost of construction, the developer’s profit, advertising costs and so on. Only about 10-15 percent of the purchase cost is in the land. So longer term the depreciation of the building will push values lower.

If you are heavily indebted, act immediately to get out of debt, even if that means selling a property at a loss. Be aggressive in pricing your property. If you have offspring in this position, don’t put more money into a losing investment.

Don’t hang on to an investment in real estate, waiting for the market to recover. In the US the market took four years to bottom, from 2006 to 2010. And that housing bubble was much less severe than this one in Canada. So, cut your losses quickly. Some people are hung up on their anchor price, a price that the property might have been worth at the peak in 2016 or 2017. Or the anchor price might be their purchase price. But with the market correcting, it’s much more important to sell quickly. Remember, the only thing that matters is the direction of prices in the future.

If you are planning to downsize into a smaller property in retirement, act sooner rather than later. In the chapter on Demographics, I point out that many baby boomers will need to sell their homes to fund retirement. The median boomer reaches 65 years old in 2019 and by 2031 one quarter of all Canadians will be older than that. That’s an increase of 4 million people!

And if you are retiring soon and could use some extra money, consider renting instead of owning. In the last four years it’s become more common to find people who are renting. Any landlord would love to have an older couple as tenants, and the costs of renting are much lower than ownership, if house prices are flat or declining.

And finally, if you are a first-time buyer, do not rush into the housing market. The correction will take years, not months. And the best bargains will appear when sellers become more realistic or when lenders start to sell the homes acquired through foreclosure. The process of liquidation of housing assets and the write-down of associated household debt is just getting started, in early 2019.

Good luck.

Hilliard MacBeth

The opinions expressed in this report are the opinions of the author and readers should not assume they reflect the opinions or recommendations of Richardson GMP Limited or its affiliates. Assumptions, opinions and estimates constitute the author's judgment as of the date of this material and are subject to change without notice. We do not warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Past performance is not indicative of future results. The comments contained herein are general in nature and are not intended to be, nor should be construed to be, legal or tax advice to any particular individual. Accordingly, individuals should consult their own legal or tax advisors for advice with respect to the tax consequences to them, having regard to their own particular circumstances.. Richardson GMP Limited is a member of Canadian Investor Protection Fund. Richardson is a trade-mark of James Richardson & Sons, Limited. GMP is a registered trade-mark of GMP Securities L.P. Both used under license by Richardson GMP Limited.